Dominic Phillips

Partner & Co-Founder

AI Is Reshaping the Revenue Cycle Conflict Between Payers and Providers

Hospitals and insurers are both deploying AI into prior authorization, claims review, and denials management. That does not just automate paperwork. It changes bargaining power, cash flow, and margin structure across healthcare.

For years, revenue cycle technology was sold as a way to reduce friction: fewer manual steps, faster claims submission, cleaner payment workflows.

That framing is now incomplete. In 2026, both sides of reimbursement are adopting AI at the same time. Providers are using it to prevent denials, accelerate appeals, and protect cash flow. Payers are using it to flag billing discrepancies, scrutinize documentation, and tighten payment controls.

This is not just an efficiency story. It is an escalation story.

When both sides automate, the system changes character. Decisions happen faster. Review volume increases. Edge cases get surfaced more aggressively. Organizations with weak data, loose workflows, and poor systems integration absorb the pain first.

The question is no longer whether AI will enter the revenue cycle. It already has. The real question is what happens when reimbursement becomes a contest between two increasingly automated operating systems.

Reimbursement is becoming a contested system

Recent reporting has made the shift harder to ignore. Reuters reported in March that insurers and hospitals are turning to new AI tools in the long-running fight over charges and payments. The significance is not the tech itself. It is that both sides now see reimbursement infrastructure as a competitive lever.

Providers are feeling the pressure directly. In Adonis's 2026 State of Revenue Cycle Management Report, nearly two-thirds of surveyed leaders said denials and underpayments had become their biggest barrier to revenue growth. The same report found that 66% view automated denial follow-up and resolution as a very important AI capability, and that more than one-third now discuss denial impact at the executive level rather than treating it as a back-office issue. The picture is clear: denials management has moved from clerical drag to strategic finance.

Policy is also raising the stakes. CMS's Interoperability and Prior Authorization Final Rule requires impacted payers to implement certain provisions by January 1, 2026, while giving most plans until January 1, 2027 to meet the API requirements. The effect is to push the industry toward more standardized electronic workflows rather than the older mix of portals, faxes, and phone calls. That does not eliminate friction. It changes where the friction lives: in digital infrastructure, data quality, response times, and workflow orchestration.

That transition is proving uneven in practice. A March 2026 Healthcare Finance News report on new WEDI survey data found that 33% of providers had not yet started work on Prior Authorization API requirements and that many respondents still cited testing coordination, internal expertise, and TEFCA, QHIN, and HIE network complexity as core implementation hurdles.

CMS's WISeR model adds another layer. CMS says the model runs from January 1, 2026 through December 31, 2031 across six states and uses enhanced technologies, including AI and machine learning, alongside human clinical review to support earlier review of selected services. The American College of Radiology's January 2026 update makes the practical point sharper: WISeR implementation is being refined through recurring operational guidance, with select Original Medicare items and services subject to prior authorization or pre-payment medical review for dates of service on or after January 15, 2026.

A separate 2026 HFMA report on denials shows how this is landing operationally. HFMA cited Kodiak Solutions data showing an 11.65% initial denial rate through November 2025, up from 11.41% in 2024, with prior authorization and precertification denials also rising. More important than the exact percentages is the directional change: denials are arriving faster, on smaller claims, and with more ambiguous logic. That pushes providers to respond with better documentation, better routing, and more systematic appeal workflows.

Strategically, this fits the broader posture entering 2026. In Deloitte's 2026 US Health Care Outlook, 80% of surveyed executives said regulatory and policy factors would influence their 2026 strategies, while only one-third said their organizations were operating AI at scale.

The old administrative mess is not disappearing. It is being formalized, instrumented, and accelerated.

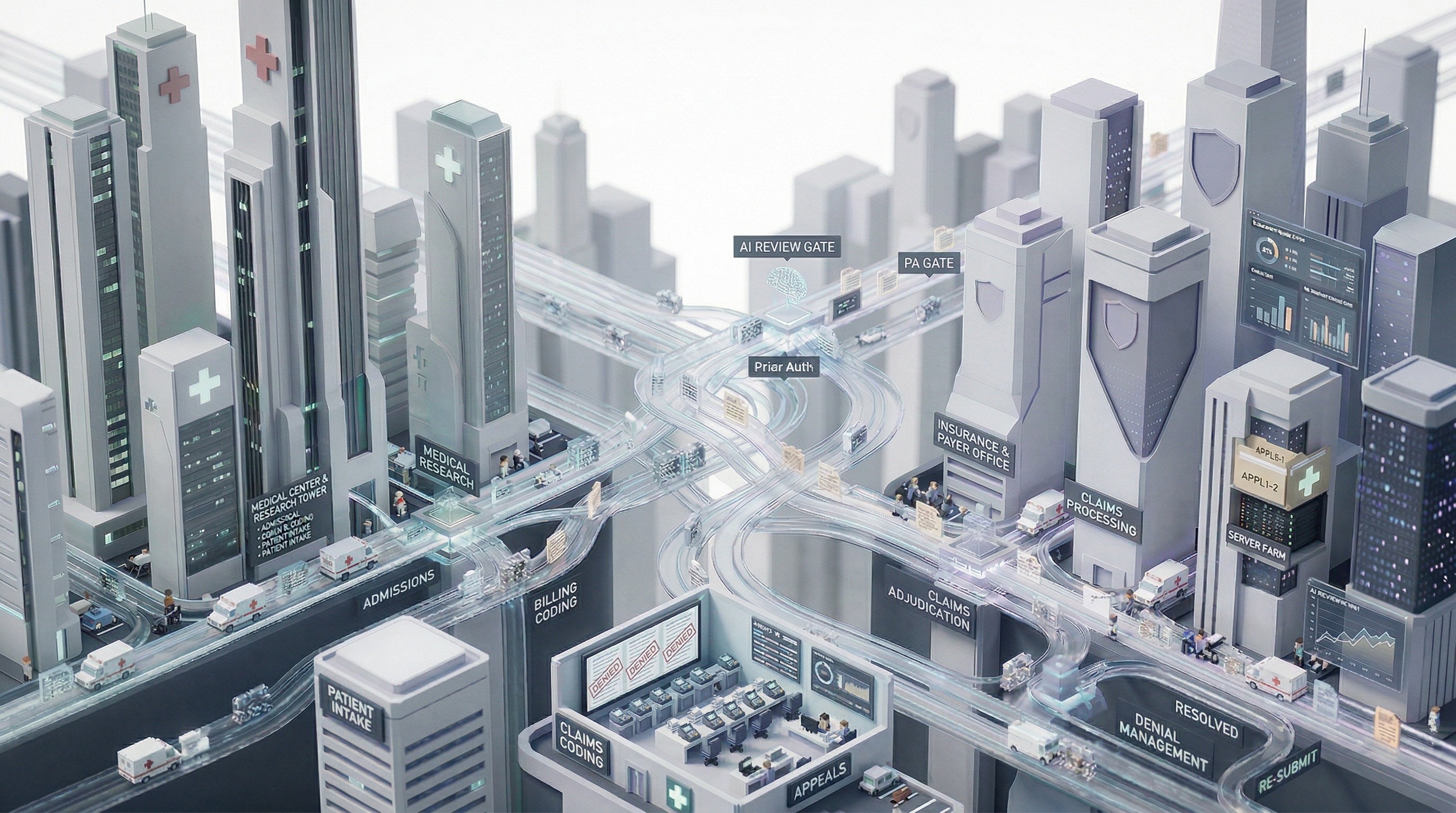

A simple view of how AI compresses cycle times on both sides of reimbursement.

The operating logic is becoming more adversarial

The simplest way to understand the market is this: providers and payers are each using AI to compress their own cycle times and improve their own economics. Those gains are not neutral. They raise the pressure on the other side to respond.

For providers, the goal is straightforward: submit cleaner claims, reduce preventable denials, shorten time to payment, and preserve margin without adding headcount.

For payers, the goal is equally straightforward: detect unsupported charges earlier, enforce policy more consistently, reduce unnecessary spend, and scale review capacity without scaling labor.

The result is a tighter operating loop:

- Faster payer review raises the standard for provider documentation and denial defense.

- Faster provider resubmissions and appeals force tighter payer adjudication and exception handling.

- As prior auth becomes more digital under the new CMS framework, laggards become easier to identify and easier to delay.

AI does not just lower unit cost. It changes the tempo and intensity of reimbursement conflict.

2026 survey data suggests denial pressure has become both a financial and automation priority for revenue leaders.

Source: Adonis 2026 State of Revenue Cycle Management Report announcement.Where the pressure shows up first

The pattern is likely to appear in four places before it becomes obvious in financial statements.

1. Prior authorization

Prior auth is the most visible battleground because it combines administrative pain, clinical nuance, and direct cash consequences. AI can help providers assemble documentation, route requests, predict approval risk, and reduce avoidable errors. On the payer side, AI can support intake, categorization, policy matching, and exception review.

As electronic prior auth becomes more standardized under CMS's Interoperability and Prior Authorization Final Rule, the competitive edge moves away from brute-force staffing and toward workflow design. Operators with fragmented systems, weak documentation capture, or poor integration between clinical and administrative teams will struggle even if they buy point solutions.

WISeR sharpens that point. Because the model explicitly combines enhanced technologies with human review for selected Medicare services, it offers a preview of what more instrumented utilization management can look like when policy and software start reinforcing each other.

HealthLeaders made a similar point in its 2026 questions for revenue cycle leaders, noting that agentic systems are increasingly being discussed for tasks like logging into payer portals and uploading medical documentation without human intervention.

2. Claims editing and denials prevention

Providers increasingly use AI upstream to catch coding mismatches, missing modifiers, and documentation gaps before claims go out the door. That can improve first-pass yield. But if payers use AI to expand scrutiny downstream, the bar rises. Denials prevention becomes less about a single tool and more about whether the organization has a coherent documentation-to-billing chain.

That is one reason the Adonis survey data matters. If denials and underpayments are now the top revenue risk for many operators, then AI adoption in claims editing is not just a productivity story. It is a margin defense story.

The same logic shows up in HFMA's reporting, which describes a market where denials are becoming smaller, sneakier, and faster. In that environment, upstream claims quality and payer-specific rules intelligence become more valuable than generic automation promises.

If a team can see denial patterns but cannot route work back into documentation, coding, or payer follow-up systems, the insight does not change cash performance. The practical work is connecting detection to action.

The shift to electronic prior auth is real, but a meaningful share of providers still appear early in the readiness curve.

Source: Healthcare Finance News reporting on March 2026 WEDI survey data.Fix the operating spine first

Most healthcare organizations are not losing margin because they lack access to AI. They are losing margin because their workflow architecture is weak. A fragmented revenue cycle cannot be saved by a thin layer of automation. If anything, AI can expose the weakness faster.

The strategic question is not, "What AI vendor should we buy?" It is, "Where does information break between clinical documentation, authorization, coding, submission, adjudication, and appeal?"

The likely outcome is not a world where reimbursement friction disappears. It is a world where capability gaps widen.

Large payers will continue investing in automated review infrastructure. Sophisticated provider groups and health systems will invest in denials prevention, documentation quality, and workflow orchestration. Under-tooled providers will face a harsher environment: more denials pressure, slower collections, heavier administrative rework, and more margin leakage hidden inside apparently digital workflows.

Strengthen the revenue cycle before it speeds up again

The immediate job is not to assemble a longer tool list. It is to strengthen the operating spine of the revenue cycle before reimbursement workflows get even faster. That starts with mapping how information actually moves from scheduling and intake through documentation, authorization, coding, claim submission, remittance, and appeal. In most organizations, leakage sits in the handoffs between teams and systems.

From there, the better investment is usually integration before intelligence. If core systems do not talk to each other cleanly, AI will mostly help bad workflows fail faster. Operators should focus first on connective infrastructure, cleaner data movement, and better instrumentation at the task and queue level. Denials should be treated as a structured operating signal, not as background noise.

Revenue cycle improvement usually depends less on adding another tool than on tightening the handoffs between systems, teams, and decisions.

The next layer is organizational learning. The revenue cycle is not one problem. It is a portfolio of payer behaviors, documentation thresholds, authorization patterns, and appeal economics. The operators that outperform will build payer-specific operating knowledge and use it to shape workflow design, staffing, and automation priorities. The measurement discipline also has to stay grounded in cash outcomes: first-pass payment rates, avoidable denials, turnaround time, labor per claim, and net collections.

Bottom line

Healthcare is entering a phase where AI is no longer just helping organizations do administrative work faster. It is changing how aggressively the reimbursement system itself operates.

When both payers and providers deploy AI into the same contested workflows, the advantage goes to the side with better data, tighter process control, and faster learning loops.

The old story was that AI would take friction out of healthcare administration. The more realistic story is that AI will redistribute that friction. Some organizations will translate it into margin and cash flow. Others will absorb it as complexity, denial pressure, and rework.

Cade Newsletter

Research that moves before the market does.

Original analysis on healthcare strategy, AI adoption, and market dynamics. Delivered when we publish.

No spam. Unsubscribe anytime.